Guest viewing is limited

- You have a limited number of page views remaining

- 9 guest views remaining

- Register now to remove this limitation

- Already a member? Click here to login

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

28 comments

MediaSeller

Member

Hello, Is this still available ?

Hi,Hello, Is this still available ?

Yes, free cards promo is still available so you should hurry up!

Have a nice day!

PST.NET provides virtual payment cards (VCC) from US and European banks with instant deposit and withdrawal operations, now offers the best conditions on the market (literally).

Up to 100 free cards for media buying teams – for testing $1 for additional cards – more than 25 BINs from 5 US & EU banks 2% card deposit fee – lowest on the market

Up to 100 free cards for media buying teams – for testing $1 for additional cards – more than 25 BINs from 5 US & EU banks 2% card deposit fee – lowest on the marketVisa Platinum Credit cards, 3D-Secure and BIN quality monitoring system from PST.NET will provide unsurpassed level of protection against problems with financial verification on all advertising platforms.

Fill out the form to get 100 free cards @Ann_PST_Private

i need one cardlate for

i need one card

Hello!

You can get your own card in couple of minutes – KYC isn't required for the first one

")

Enjoy PST.NET!

The best conditions on virtual cards market from PST.NET!

Premium cards (Visa Platinum Credit), 3D-Secure support and BIN quality monitoring system will help you easily make foreign purchases and pay for online advertising expenses.

We worked hard to provide you with the best conditions on the market – up to 100 free cards for the test, from $1 per card and from 2% top-up commission.

Virtual Payment Card Service PST.NET is a best option for teamwork – Master accounts can manage the team structure and the limits for each participant, as well as set up expense categories and download reports.

The best offer on the virtual card market is waiting for you!

Mandy Kotlyar

New Member

Their Private program swayed me to join, and I'm loving the terms guys offered me

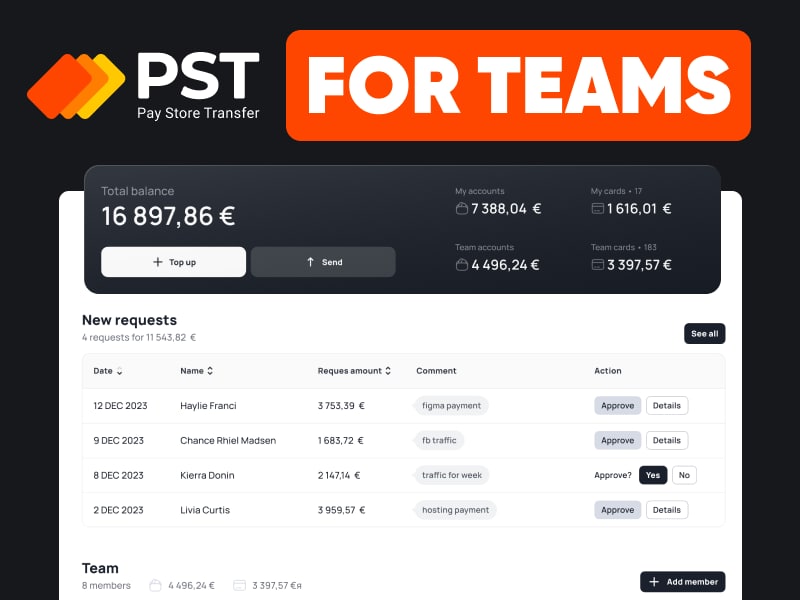

Working as a team? Meet tools for teamwork from PST.NET virtual card payment service!

Working as a team? Meet tools for teamwork from PST.NET virtual card payment service!Teamwork capabilities:

Employee management: invitation and suspension, role change Setting spend limits Instant transfer of cards and funds between team accountsTop-up request system Transaction history for all participants, reports in CSV format

Employee management: invitation and suspension, role change Setting spend limits Instant transfer of cards and funds between team accountsTop-up request system Transaction history for all participants, reports in CSV formatSoon: Spend forecast system

Soon: Setting allowed merchant categories

To get the Master account status contact our customer care service

To get the Master account status contact our customer care service

Affiliate Mythology, Part I. How to choose a virtual payment card in 2023?

In their professional activities, affiliate marketers often rely not only on their own experience but on market-established beliefs as well. It is often difficult to determine which of these beliefs are true and relevant, and which are trivial myths. Our guest experts will help us with separating the grains of truth from the husks of myths, and will share with us their thoughts on each such tenet. We will begin our delve into affiliate mythology with a very sensitive topic that became especially hot last year - we will talk about payment cards for affiliate marketing in 2023. Danya, co-founder of Grats Group, has recently published a very interesting article comparing popular virtual payment cards (add link) and today he’s gonna help us prove or bust some of the affiliate marketing myths about payments.

– Hey, Danya! Thanks for taking the time for a talk. Quick question: did you come across affiliate marketing myths about payments in your daily work?

– Hi! Thanks for having me My favorite one is "card trust depends on the balance" – this was from our trainee. He did not work with us already

– Why so? Are you sure it's a myth?

– I don't know about the effect on a trust, but my mood definitely depends on the balance of my card

– Seriously, do you have a theory about where all these myths are coming from?

– It's pretty straightforward. Affiliate marketing is such a turbulent process with so many variables so people have to believe at least in some patterns.

– That sounds reasonable. Do you know any other myths about VCC?

– In my experience, all the myths about payment cards come down to one simple question: are the cards trustworthy? The funny part is that no one really elaborates on the meaning of "trusted payment cards" or even on the results that are expected from them.

– Word "trust" is on everyone's lips lately, so let's try to figure out the meaning together. Let me remind the format of our materials for our readers: we will ask our guests about the myths we have found and our guests will tell their thoughts and give their verdict: is it true or false. So, here we go.

Myth #1: There is no such thing as trusted payment cards, it all depends on the quality of the advertising accounts.

– It is easy to argue with this statement. Even general understanding of antifraud mechanisms on advertising platforms is enough to bust that myth. Analytics of bigtech giants like Facebook or Google are based on neural networks that constantly process huge amounts of data in search of correlations. Detected correlations are used both for advertising purposes (for targeting) and for banning unwanted users (political provocateurs, spammers and affiliate marketers, especially first-billers*). Ad platforms have access to all payment data of all users, so AI easily find similarities in BINs** associated with "unwanted" accounts. Soon after, trust of those BINs goes down, and the number of risk-payment bans increases. Even if a person ties a clean, brand new card (but with a blacklisted BIN) to an advertising account, advertising platforms quickly detect it, score and come up with the verdict: "you may be ready to pay us, but we don't want your money". Then restrictions are imposed on such an account. So for me (and for the people I trust), that statement is a myth.

– So, if trusted payment cards exist, where to find them?

– Media buyers should follow one of two strategies in their search for trusted payment cards: to use either cards from major banks or cards with exclusive BINs. In the first case media buyers can cloak their activities behind a huge number of other bank clients, and in the second case stability is achieved by the absence of negative records for a rare BIN in the antifraud systems of advertising platforms.

Checking a BINs is a rule for all members in our team, because we strive to choose cards with high credit status, like Visa Infinite / Mastercard World Elite or Platinum cards. It’s possible that we have made up a myth for ourselves, but so far our experience shows that such cards work better. We check our cards and their BINs at pulse.pst.net, as guys from PST have made a great tool for that. In addition to the standard functionality of BIN checkers, they disclose information about the current performance of their BINs in real time (percentage of approved and declined transactions, average spend per card and billing thresholds).

– I haven't heard about such features of BIN-checkers yet, so I'll check it out. Ok, let's move on and define the next myth as follows:

Myth #2: 3D-Secure support makes cards more resistant to bans and at the same time increases the possible spending limits.

– It is important to remember that there are services that are impossible to pay for without 3DS (for example, Hetzner servers). In such cases, the necessity of 3DS support is non-negotiable. But for Google Ads or Facebook Ads confirmation codes from SMS are purely optional. From my experience, this is more of a myth. There is practically no difference in spending limits between solutions with 3DS and without 3DS.

To get a virtual card with 3DS is a painful process on many payment services. Plus it may be hard to get 3DS confirmation codes from their support specialists. In some cases when such codes have to be obtained manually, setting up ad accounts can take so much time that it just becomes impractical. Although there are services that send confirmation codes via Telegram bot, such as the one of PST guys.

– Situation with 3DS makes more sense now, thank you. Next we have the myth about geo:

Myth #3: Geo of a bank that issued payment card and ad account geo have to match for more trust.

– We use cards from US banks. When paired with US ad accounts our results were slightly better than with ad accounts from other countries – spending limit difference peaked at 15%. Yet we can’t be sure that this is not a statistical error. In this case, the main criteria for selecting any payment cards is often their cost, which directly affects the profitability of all affiliate activities. You can buy US FB accounts for $30, on average, and the price of good Vietnamese accounts is around $5.

Anyway, even a 15% increase in spending limits (which no one guarantees) does not justify the higher cost of cards from US banks. In short, I have no hard evidence, so I'll consider this statement a myth

– That's cool, one more myth is busted. Is there anything else to share about the mythology of virtual payment cards for affiliate marketing?

– Let’s bust the myth of the connection between card balance and card trust once and for all. Just for understanding: not a single acquiring service, not even giants like Google and Facebook, can ever get data on someone’s card balance, it just doesn’t work like that. Simply by the fact that financial data falls under the privacy policy, so it's a 100% myth. Surprisingly banks cannot even identify the real card holder, which is a definite plus for affiliate marketers. Otherwise, antifraud systems would work even more accurately and harshly. When entering payment info in facebook, our team always uses first and last names from social accounts. We assume this is our personal prejudice, but we take it as a digital cleanliness of some kind. Plus, if it doesn't take a lot of time from us and definitely doesn't hurt the outcome, I don't see the reason in not doing so.

– Agreed, I think traditions appear in any team sooner or later. By the way, can you share some payment insights with our readers?

– If we move away from mythology to practice, then every marketer always faces the need of optimisation – f.e. choosing the best service provider, including payment ones.

My team and I have learned a lot, so I guess we have a lot to share.

First of all, if we talk about the work of an affiliate marketing or media buying team (even a medium-sized one) we are talking about the necessity of constantly depositing turnover money into payment services' accounts. In the past year, we all have seen that even Tier-1 banks were involved in prosecutions, so what should we expect from payment solutions for affiliate marketing?

Obviously, there is always a risk, that’s why we don’t want to cooperate with “messenger-only” payment services and ones without an official bank API. We know too well that the work of such services can stop at any time (hello, BankOff).

Although bank API is not a panacea either, we choose only such services. The logic is simple, as each service has already paid $100-150k to Visa or Mastercard for the opportunity to work via API, so it drastically reduces the risk of scam. Earlier we tried to use several payment systems at once, but eventually we got tired of facing the same problems.

Now we have come to the point where we choose one provider, but we do it thoroughly – we study the history, the dynamics of product development, the frequency of updates, and other objective indicators.

Second, we strongly recommend that you read ALL the terms and conditions of your payment vendor. Popular solution for additional monetization from such payment services is the trick with decline rate and FB transaction fees. Once we were tempted by good conditions, which in fact turned out to be much worse (the real commission was 12% instead of the declared 4%)

Third, the variability and quality of BINs. Everything is clear here: more BINs equals lower chances of getting payment bans.

And last but not least: interface usability and customer support’s time to react. It is always nice when the UI corresponds to current market standards, like banking apps we are used to. Yet any affiliate marketer will not care much about that, they just need not to get scammed.

– Finally, can you list the recommended payment services for our readers?

– Well, there's not much to list, really. If it weren’t for commissions, I would look at the authority of the payment service. One of the most respected ones on the market are Capitalist and MyBrocard, but in the end, all our needs were satisfied by PST.NET service (they also have a referral program). They are just dumping the market with their Private program, but to get there one needs to show at least $30k monthly spend. On the other hand they can provide users with the best terms on the market right now: 100 free cards for the test (then $1 for a card) and top-up commission starting from 2%.

– Great, the myths were busted and now we have your recommendations on payment cards for affiliate marketing, I hope our readers will be happy. Thanks again, you are welcome to join us in our new materials!

– Drop me a call, I’m interested to talk more on such topics myself

See you around!

* First billers - not-so-nice guys, who’s business model is to pay the first small advertisement bill from Facebook and not compensate the following ones as FB allows post-factum payment.

** BIN (Bank Identification Number) – first 6 digits of any payment card that can be used for getting various data about the payment card. BIN-checkers are websites where users can get a lot of information by entering the BIN:

In their professional activities, affiliate marketers often rely not only on their own experience but on market-established beliefs as well. It is often difficult to determine which of these beliefs are true and relevant, and which are trivial myths. Our guest experts will help us with separating the grains of truth from the husks of myths, and will share with us their thoughts on each such tenet. We will begin our delve into affiliate mythology with a very sensitive topic that became especially hot last year - we will talk about payment cards for affiliate marketing in 2023. Danya, co-founder of Grats Group, has recently published a very interesting article comparing popular virtual payment cards (add link) and today he’s gonna help us prove or bust some of the affiliate marketing myths about payments.

– Hey, Danya! Thanks for taking the time for a talk. Quick question: did you come across affiliate marketing myths about payments in your daily work?

– Hi! Thanks for having me

My favorite one is "card trust depends on the balance" – this was from our trainee. He did not work with us already– Why so? Are you sure it's a myth?

– I don't know about the effect on a trust, but my mood definitely depends on the balance of my card

– Seriously, do you have a theory about where all these myths are coming from?

– It's pretty straightforward. Affiliate marketing is such a turbulent process with so many variables so people have to believe at least in some patterns.

– That sounds reasonable. Do you know any other myths about VCC?

– In my experience, all the myths about payment cards come down to one simple question: are the cards trustworthy? The funny part is that no one really elaborates on the meaning of "trusted payment cards" or even on the results that are expected from them.

– Word "trust" is on everyone's lips lately, so let's try to figure out the meaning together. Let me remind the format of our materials for our readers: we will ask our guests about the myths we have found and our guests will tell their thoughts and give their verdict: is it true or false. So, here we go.

Myth #1: There is no such thing as trusted payment cards, it all depends on the quality of the advertising accounts.

– It is easy to argue with this statement. Even general understanding of antifraud mechanisms on advertising platforms is enough to bust that myth. Analytics of bigtech giants like Facebook or Google are based on neural networks that constantly process huge amounts of data in search of correlations. Detected correlations are used both for advertising purposes (for targeting) and for banning unwanted users (political provocateurs, spammers and affiliate marketers, especially first-billers*). Ad platforms have access to all payment data of all users, so AI easily find similarities in BINs** associated with "unwanted" accounts. Soon after, trust of those BINs goes down, and the number of risk-payment bans increases. Even if a person ties a clean, brand new card (but with a blacklisted BIN) to an advertising account, advertising platforms quickly detect it, score and come up with the verdict: "you may be ready to pay us, but we don't want your money". Then restrictions are imposed on such an account. So for me (and for the people I trust), that statement is a myth.

– So, if trusted payment cards exist, where to find them?

– Media buyers should follow one of two strategies in their search for trusted payment cards: to use either cards from major banks or cards with exclusive BINs. In the first case media buyers can cloak their activities behind a huge number of other bank clients, and in the second case stability is achieved by the absence of negative records for a rare BIN in the antifraud systems of advertising platforms.

Checking a BINs is a rule for all members in our team, because we strive to choose cards with high credit status, like Visa Infinite / Mastercard World Elite or Platinum cards. It’s possible that we have made up a myth for ourselves, but so far our experience shows that such cards work better. We check our cards and their BINs at pulse.pst.net, as guys from PST have made a great tool for that. In addition to the standard functionality of BIN checkers, they disclose information about the current performance of their BINs in real time (percentage of approved and declined transactions, average spend per card and billing thresholds).

– I haven't heard about such features of BIN-checkers yet, so I'll check it out. Ok, let's move on and define the next myth as follows:

Myth #2: 3D-Secure support makes cards more resistant to bans and at the same time increases the possible spending limits.

– It is important to remember that there are services that are impossible to pay for without 3DS (for example, Hetzner servers). In such cases, the necessity of 3DS support is non-negotiable. But for Google Ads or Facebook Ads confirmation codes from SMS are purely optional. From my experience, this is more of a myth. There is practically no difference in spending limits between solutions with 3DS and without 3DS.

To get a virtual card with 3DS is a painful process on many payment services. Plus it may be hard to get 3DS confirmation codes from their support specialists. In some cases when such codes have to be obtained manually, setting up ad accounts can take so much time that it just becomes impractical. Although there are services that send confirmation codes via Telegram bot, such as the one of PST guys.

– Situation with 3DS makes more sense now, thank you. Next we have the myth about geo:

Myth #3: Geo of a bank that issued payment card and ad account geo have to match for more trust.

– We use cards from US banks. When paired with US ad accounts our results were slightly better than with ad accounts from other countries – spending limit difference peaked at 15%. Yet we can’t be sure that this is not a statistical error. In this case, the main criteria for selecting any payment cards is often their cost, which directly affects the profitability of all affiliate activities. You can buy US FB accounts for $30, on average, and the price of good Vietnamese accounts is around $5.

Anyway, even a 15% increase in spending limits (which no one guarantees) does not justify the higher cost of cards from US banks. In short, I have no hard evidence, so I'll consider this statement a myth

– That's cool, one more myth is busted. Is there anything else to share about the mythology of virtual payment cards for affiliate marketing?

– Let’s bust the myth of the connection between card balance and card trust once and for all. Just for understanding: not a single acquiring service, not even giants like Google and Facebook, can ever get data on someone’s card balance, it just doesn’t work like that. Simply by the fact that financial data falls under the privacy policy, so it's a 100% myth. Surprisingly banks cannot even identify the real card holder, which is a definite plus for affiliate marketers. Otherwise, antifraud systems would work even more accurately and harshly. When entering payment info in facebook, our team always uses first and last names from social accounts. We assume this is our personal prejudice, but we take it as a digital cleanliness of some kind. Plus, if it doesn't take a lot of time from us and definitely doesn't hurt the outcome, I don't see the reason in not doing so.

– Agreed, I think traditions appear in any team sooner or later. By the way, can you share some payment insights with our readers?

– If we move away from mythology to practice, then every marketer always faces the need of optimisation – f.e. choosing the best service provider, including payment ones.

My team and I have learned a lot, so I guess we have a lot to share.

First of all, if we talk about the work of an affiliate marketing or media buying team (even a medium-sized one) we are talking about the necessity of constantly depositing turnover money into payment services' accounts. In the past year, we all have seen that even Tier-1 banks were involved in prosecutions, so what should we expect from payment solutions for affiliate marketing?

Obviously, there is always a risk, that’s why we don’t want to cooperate with “messenger-only” payment services and ones without an official bank API. We know too well that the work of such services can stop at any time (hello, BankOff).

Although bank API is not a panacea either, we choose only such services. The logic is simple, as each service has already paid $100-150k to Visa or Mastercard for the opportunity to work via API, so it drastically reduces the risk of scam. Earlier we tried to use several payment systems at once, but eventually we got tired of facing the same problems.

Now we have come to the point where we choose one provider, but we do it thoroughly – we study the history, the dynamics of product development, the frequency of updates, and other objective indicators.

Second, we strongly recommend that you read ALL the terms and conditions of your payment vendor. Popular solution for additional monetization from such payment services is the trick with decline rate and FB transaction fees. Once we were tempted by good conditions, which in fact turned out to be much worse (the real commission was 12% instead of the declared 4%)

Third, the variability and quality of BINs. Everything is clear here: more BINs equals lower chances of getting payment bans.

And last but not least: interface usability and customer support’s time to react. It is always nice when the UI corresponds to current market standards, like banking apps we are used to. Yet any affiliate marketer will not care much about that, they just need not to get scammed.

– Finally, can you list the recommended payment services for our readers?

– Well, there's not much to list, really. If it weren’t for commissions, I would look at the authority of the payment service. One of the most respected ones on the market are Capitalist and MyBrocard, but in the end, all our needs were satisfied by PST.NET service (they also have a referral program). They are just dumping the market with their Private program, but to get there one needs to show at least $30k monthly spend. On the other hand they can provide users with the best terms on the market right now: 100 free cards for the test (then $1 for a card) and top-up commission starting from 2%.

– Great, the myths were busted and now we have your recommendations on payment cards for affiliate marketing, I hope our readers will be happy. Thanks again, you are welcome to join us in our new materials!

– Drop me a call, I’m interested to talk more on such topics myself

See you around!

* First billers - not-so-nice guys, who’s business model is to pay the first small advertisement bill from Facebook and not compensate the following ones as FB allows post-factum payment.

** BIN (Bank Identification Number) – first 6 digits of any payment card that can be used for getting various data about the payment card. BIN-checkers are websites where users can get a lot of information by entering the BIN:

- Payment system: Visa, Mastercard, МИР, UnionPay and more

- Card type: debit, credit, classic, gold, platinum, etc

- Issuing bank and country of registration and more

SemiRetired

Active Member

$120+/year?! No thanks.

Hi! The overall sum for the yearly maintenance may vary as there are different card types with monthly fees less than $10 and we offer special conditions for teams and individuals with monthly spending above $10k, where cards' and transactions' fees are even lower. Besides, we believe that even $10 is reasonable price for reliable cards with trusted US BINs that provide seamless workflow on add platforms. Contact our customer care service and we definitely can work out something!$120+/year?! No thanks.

SemiRetired

Active Member

Og god, you are spamming my inbox every fucking day with some nonsense email crap.

"Problems?"

"Get $250 for your opinion"

"Scam alart"

"Personal offer from CEO"

"Pet the cat"

I regret sigining up with you. How do I delete my account?

"Problems?"

"Get $250 for your opinion"

"Scam alart"

"Personal offer from CEO"

"Pet the cat"

I regret sigining up with you. How do I delete my account?

Hi,We do not recommend using this service. Hidden rules that are not provided in Terms of Service instead hidden in FaQ. Avoid at all cost.

Sorry to hear that you had such problems, but verification with documents from your country is not available right now. There are restrictions from our partner banks and we must comply with the laws of all jurisdictions in which our service operates.

We don’t hide anything from our customers, terms of service and FAQ are always in their sight.

Thank you for you feedback

Post automatically merged:

Hi,Og god, you are spamming my inbox every fucking day with some nonsense email crap.

"Problems?"

"Get $250 for your opinion"

"Scam alart"

"Personal offer from CEO"

"Pet the cat"

I regret sigining up with you. How do I delete my account?

It’s a pity you have been disappointed with our emails, we were trying to make them useful for our customers. You can easily unsubscribe with a single press of a button – we have that kind of button in every letter.

Thank you for you feedback

@PSTnet There is no a single word in your ToS that you don't support certain countries. It's only mentoined in your FaQ however you cannot access FaQ if you're not logged in. So you can only become aware of that fact after you register account which is not nice. This should be mentoined in your Terms Of Service instead of FaQ since FaQ is not a legal document while Terms of Service is.

Sounds reasonable, we will think about possible improvements of our documents.@PSTnet There is no a single word in your ToS that you don't support certain countries. It's only mentoined in your FaQ however you cannot access FaQ if you're not logged in. So you can only become aware of that fact after you register account which is not nice. This should be mentoined in your Terms Of Service instead of FaQ since FaQ is not a legal document while Terms of Service is.

Thank you for the idea!